The Gulf Coast Illusion:

The nation’s implicit fuel insurance policy is being sold overseas and nobody is watching the balance sheet.

By Mothusi Pahl, Hartwell & Loche.

This is the first in a series on the attention gap in American fuel supply governance.

Executive Summary

The Gulf Coast Illusion examines a critical but largely unaddressed vulnerability in the United States’ fuel system – the assumption that surplus Gulf Coast refining capacity will consistently provide a reliable buffer against supply disruptions. This surplus, alongside fuel inventories and the Strategic Petroleum Reserve, has functioned as a de facto fuel security framework. However, it is not formally defined, measured, or assigned to any single institution for oversight.

The report finds that this margin of safety is being eroded by two structural trends. First, a growing share of refined product is being exported to higher-value international markets, redirecting capacity away from domestic use. Second, the U.S. refining fleet is aging and consolidating, reducing overall capacity. Together, these dynamics are narrowing the system’s ability to absorb shocks that it historically managed with relative ease.

Recent global disruptions, including the 2026 Strait of Hormuz crisis, highlight the consequences of this shift. As international demand intensifies, U.S. refining output is increasingly drawn into global markets, raising questions about how much capacity remains available to meet domestic needs. Yet no federal or state entity is tasked with evaluating whether current conditions provide adequate coverage for U.S. fuel demand under stress.

The report identifies a broader governance gap. While legal authorities exist to intervene in fuel markets during emergencies, there is no framework to define when intervention is necessary. At the same time, the regulatory environment does not create a domestic supply obligation for refiners, reinforcing a system where export decisions are driven entirely by market signals rather than national resilience considerations.

This gap extends beyond consumer fuel markets to national security. U.S. military operations rely on the same commercial supply chains, but there is no integrated assessment of their resilience under tightening capacity conditions or increased export competition.

The core finding is that the United States faces not an immediate shortage of fuel, but a lack of institutional clarity and accountability. Domestic fuel supply adequacy has never been clearly defined, and as a result, it is not systematically measured or managed. Strengthening resilience will require establishing clear responsibility for monitoring supply conditions, defining adequacy thresholds, and enabling earlier, more informed decision-making before disruptions escalate.

I. The Illusion in Real Time

In January 2026, Gulf Coast refineries were running at roughly 85 percent utilization, down from approximately 93 percent a year earlier.[1] The United States was exporting approximately 6.3 million barrels per day of refined products to Latin America, Europe, and Asia at near-record volumes.[2] The Gulf Coast refining complex was continuing what it has done for a decade: Converting cheap domestic crude into exportable product at margins that make every loaded tanker more profitable than a domestic delivery.

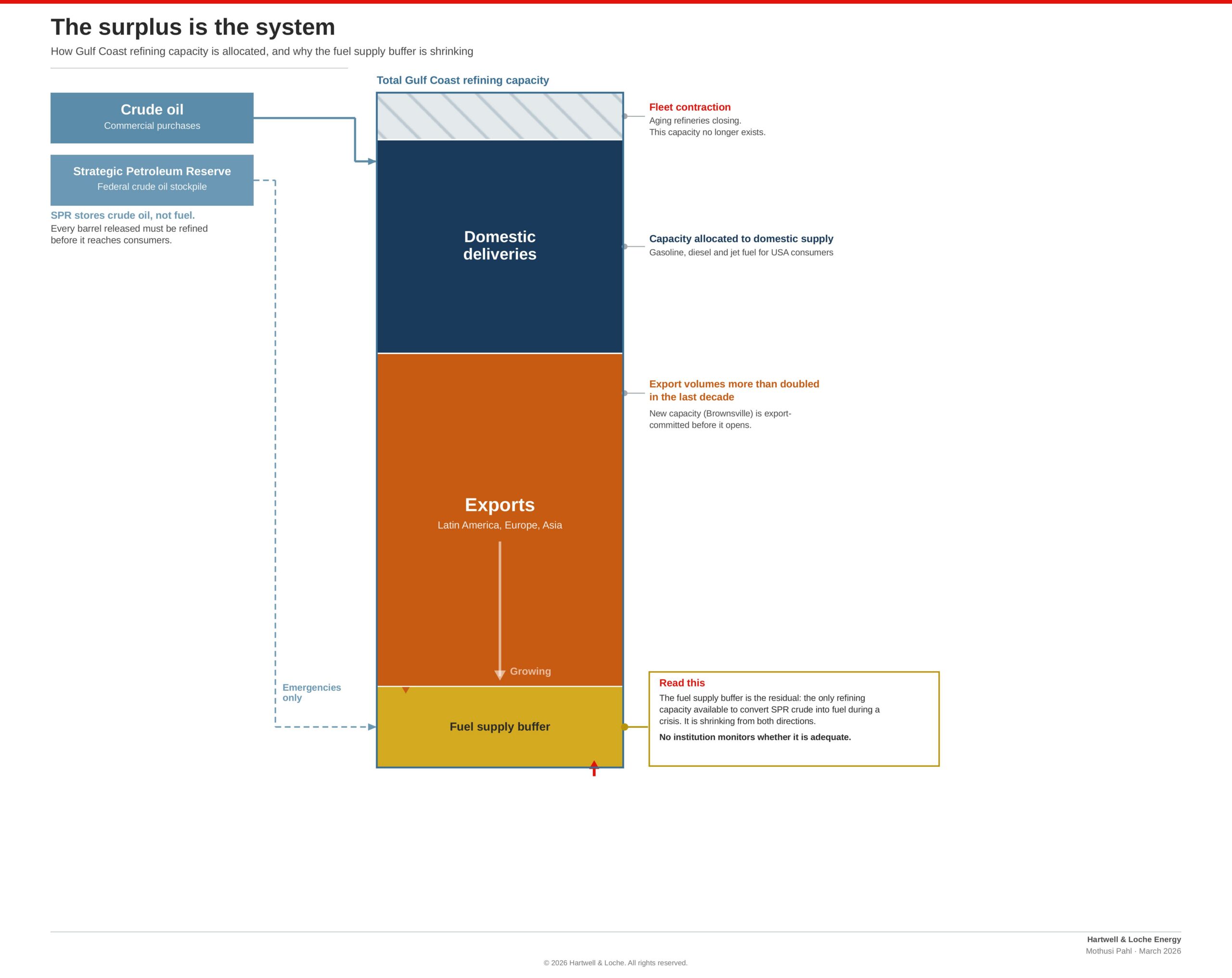

The same 10 million barrels per day of Gulf Coast refining capacity[3] that makes these exports possible is also the country’s implicit insurance against fuel supply disruption. This insurance is captured in three distinct elements: Refining capacity surplus is the headroom between what Gulf Coast refineries can process versus what the domestic market consumes. Fuel supply buffer is the surplus gasoline and diesel that provides the ability to absorb a shock. The Strategic Petroleum Reserve (SPR) is the federally owned stockpile of crude oil stored along the Gulf Coast. Together these three elements constitute the country’s fuel security architecture, and no single institution is assessing whether the balance between the three is adequate.

This absence of institutional attention did not matter as long as the national refining capacity surplus was large enough to cover every disruption the system faced. And for decades, it was: The surplus absorbed hurricanes, wars, and price spikes. But the 2026 Persian Gulf crisis is testing that capacity at an unprecedented scale. Twenty percent of global oil supply[4] is physically blocked behind a single chokepoint.

International buyers who lost their crude imports are now competing for American Gulf Coast product. When the Strait of Hormuz closed in early March, Brent crude spiked from the low $60s to $126 a barrel,[5] and the U.S. Gulf Coast refining complex became the world’s most important swing supplier. The United States’ refining capacity surplus that had long backstopped domestic fuel supply was being bid away, and no one could gauge how much of the surplus capacity remained.

One question should have been asked before any of this happened: Was anyone monitoring the Gulf Coast refining surplus, its size, its trajectory, its adequacy against a major global disruption?

The answer to all of these is no. Not the Energy Information Administration, which tracks export volumes, refinery utilization and inventory levels but has no mandate to assess whether those numbers add up to an adequate domestic supply position. Not the Office of Cybersecurity, Energy Security, and Emergency Response, which coordinates federal response during crises but does not monitor the trajectories that produce those crises. The refining capacity surplus that serves as America’s de facto fuel supply insurance has no institutional owner and no monitoring framework. It was never a policy; it was an assumption. The Persian Gulf crisis is now testing what that assumption is worth.

II. The Refining Surplus Everyone Assumed Would Last

For decades the reason no one worried was simple: So much refining capacity was concentrated along the Texas and Louisiana coast, connected by pipeline to the Midwest, the East Coast, and the Southeast, that any single disruption could be absorbed by the remaining capacity.

When Hurricane Harvey shut down more than 3 million barrels per day of Gulf Coast refining in 2017,[6] the system self-healed within weeks because surplus capacity at undamaged facilities absorbed the loss. It was the largest single disruption the Gulf Coast refining system had ever faced, and the system passed. That success should have prompted the next question: Could the same capacity buffer absorb a global supply shock five times that size? No institution, to our knowledge, ever ran that test, because no institution owns the task.

The refining capacity surplus is being eroded through two distinct mechanisms. The first is redirection: The refining capacity still exists, but the output leaves the country. The second is contraction: The refining capacity itself is being destroyed.

Redirection of Gulf Coast refinery outputs has been underway for more than a decade. Refined product exports from the Gulf Coast more than doubled from approximately 1.3 million barrels per day in 2009 to roughly 2.7 million barrels per day by 2025.[7] That growth was the rational response of a refining complex with access to cheap feedstock, deep-water export terminals, and a global market willing to pay more than domestic buyers.

The trajectory of that fuel output is now being locked-in structurally. In March 2026, America First Refining, a new U.S. refining venture, announced the first greenfield refinery in the United States in fifty years.[8] The 160,000 barrel-per-day facility at the Port of Brownsville was purpose-built for light Permian crude. India-based Reliance Industries signed a 20-year offtake agreement to purchase at least 80 percent of the facility’s refined output.[9] The Brownsville refinery does not rebuild any domestic refining surplus. It converts America’s foundational energy resource into refined product and exports it.

Redirection alone would be manageable if the refining fleet that generates the surplus were stable.

It is not.

The refining fleet is aging and consolidation is accelerating. The surplus that underwrites domestic resilience is contracting at the same time that global demand for Gulf Coast product is expanding.

Both redirection and contraction are visible in publicly available data. But no federal agency tracks whether the refining surplus is large enough to cover domestic needs after exports. No institution runs forward-looking analysis of the surplus’s adequacy against the range of supply shocks the system might face. No state regulator has the data or the mandate to model what happens when the Gulf Coast refining surplus drops below the threshold needed to absorb the next major disruption.

The threshold itself has never been formally quantified, not because the arithmetic is difficult but because no institution has been assigned to do it. The absence of the number is not a data gap. It is an institutional failure.

This failure did not become apparent until the Hormuz crisis sent international buyers scrambling for every available non-Persian-Gulf barrel, and the Gulf Coast refining surplus that had long covered domestic shortfalls became a choice prize in the global competition for fuel.

If no institution has defined domestic fuel supply adequacy as a problem requiring measurement, the question is why? The answer begins with who benefits from the absence.

Gulf Coast refiners are profit-maximizing corporations selling into a global market. Selling refined product to the highest bidder is not a failure of the system; it is the system working as designed. Refiners define domestic fuel supply as a problem when regulation constrains their ability to produce. They do not define it as a problem when exports are flowing to the highest bidder. When conditions change, as they always do in energy markets, no institution will detect the problem early or act in advance, because the baseline, analytical framework, and authority to act were never built.

III. No Domestic Supply Obligation

The United States does not lack statutory tools that could be relevant to a supply crisis. It lacks the institutional capacity to define what adequate domestic fuel supply looks like and therefore to recognize when that adequacy is eroding.

The explanation has three layers: Legal authorities that exist but have never been used, a regulatory environment that creates no domestic supply incentive, and a structural dynamic in which the existence of those unused authorities may itself be the reason the monitoring institution was never built.

Layer 1: The authorities that exist on paper

The Energy Policy and Conservation Act gave the President authority to act on petroleum product exports in 1975. The 2015 Consolidated Appropriations Act repealed Section 103 in its entirety to lift the crude oil export ban; a savings clause preserved presidential authority to intervene under other statutes, but whether those alternatives provide an effective mechanism for refined product exports has never been tested.[10]

The International Emergency Economic Powers Act (IEEPA) gives the President authority to intervene in virtually any export during a declared national emergency, but it has never been invoked for refined product exports.[11] The Defense Production Act provides a more targeted mechanism: Under 10 CFR Part 221, the DoD can request a priority rating that requires suppliers to fulfill military fuel orders before all commercial customers.[12] This has never been invoked.

Taken together, these three authorities represent substantial unused power. The legal tools exist. What does not exist is any definition of the conditions that would warrant using them.

Layer 2: Why the regulatory environment creates no domestic supply obligation

The regulatory environment gives no market participant reason to consider domestic supply adequacy.

No Gulf Coast refiner maintains a compliance function for domestic supply obligation. The question of whether such an obligation attaches to export decisions has, to our knowledge, never been a factor in commercial planning. Refined petroleum products are classified EAR99 under the Export Administration Regulations:[13] No license required. No restrictions. No notification to any federal agency. A Gulf Coast refiner can load a tanker with gasoline or diesel or jet fuel and ship it anywhere in the world with the same paperwork as a domestic delivery.

The Brownsville permitting process demonstrates this point. The project’s permits were granted under the name Element Fuels in 2024.[14] The approval evaluated environmental compliance, construction readiness and operational design. It did not evaluate, and had no mandate to evaluate, whether the facility’s output would serve domestic supply or leave the country. The 20-year offtake agreement committing 80 percent of production to India was a commercial term, not a regulatory consideration. No entity in the approval chain was assigned the question: Does this capacity serve U.S. domestic resilience?

The regulatory classification and the permitting framework both point to the same structural gap, and the political system offers no corrective. Since 2015, senior administration officials have publicly considered restricting refined product exports three times; each time the threat was withdrawn. Export decisions remain purely economic: If the netback from shipping diesel to Rotterdam exceeds the domestic rack price minus logistics cost, the cargo goes to Rotterdam.

Layer 3: The moral hazard

The question here is not whether to restrict exports; restriction would destroy refiner margins and shrink the very surplus it was meant to protect. The question we are proposing is why the monitoring capacity that would make restriction unnecessary has never been built?

The authorities described in Layer 1 are not merely unused. They are dormant, and their dormancy may itself be the reason the monitoring institution was never built. The mechanism is a classic moral hazard: The existence of emergency powers reduces the political incentive to build the proactive monitoring capacity that would make them unnecessary. The political system believed it had a backstop, so it never invested in prevention.

The 2025 Persian Gulf crisis is demonstrating this moral hazard in real time. Within days of the Strait of Hormuz closing, policymakers in the U.S. began improvising responses they had never rehearsed: new Jones Act waivers, export restrictions, Strategic Petroleum Reserve releases. Every one of these is an ad hoc, reactive measure and the predictable output of a governance structure that invested in emergency powers rather than prevention.

The Strategic Petroleum Reserve illustrates the structural mismatch most clearly. The SPR held approximately 415 million barrels as of mid-March 2026, roughly 57 percent of its capacity, and the administration announced a 172 million barrel release on March 12.[15] But the SPR stores crude oil, not refined products. An SPR release puts crude into the market that must be processed through the same Gulf Coast refineries this analysis has described as shrinking and export-committed. The SPR is a crude oil supply tool being deployed into a refining capacity constraint that no institution has modeled.

Japan offers a definitive contrast to this entire structure. Japanese refiners hold 70 days of commercial petroleum inventory because the law requires it and the Ministry of Economy, Trade and Industry enforces it with inspection authority and penalties that include imprisonment.[16] Japan built that system after the 1973 oil shock and has had fifty years to mature it. The United States has dormant crisis authorities that create no behavioral change in normal times. This is the difference between a real domestic supply obligation and a theoretical one. Japan’s system was designed to prevent the crisis. Ours was never designed at all.

IV. The Military Dependency Nobody Assessed

The cost of this absence is not limited to consumer fuel prices. It extends to the military installations that depend on the same civilian supply chains no institution is monitoring.

Military installations across the Pacific depend entirely on civilian fuel supply chains for their operational fuel.[17] The Defense Logistics Agency’s energy arm, DLA-Energy, contracts for fuel delivery as a commodity purchase but does not assess the structural resilience of the supply chain underneath. The assumption is the same one this analysis has described eroding: That the Gulf Coast will continue to produce fuel at the volumes the military requires.

The DoD has one legal tool for fuel supply crises, but its design reveals a parallel problem. The priority supply authority at 10 CFR Part 221 gives DoD the legal mechanism to demand that suppliers fulfill military fuel orders before commercial customers, but it has never been invoked. The reason is that there is no mechanism to determine when invocation is needed. The priority supply authority is a “last mile” authority: It can compel delivery once a crisis is recognized. But DoD has no “first mile” intelligence system for recognizing that the conditions for a fuel supply crisis are forming.

Hawaii illustrates the exposure most concretely. The state’s military installations, including Pearl Harbor and Joint Base Pearl Harbor-Hickam, depend on a fuel supply chain that ultimately traces to a single refinery: Par Hawaii.[18] The military’s own backup, the Red Hill Bulk Fuel Storage Facility, was defueled and closed in 2024 following a contamination crisis.[19] As a result, Hawaii’s military fuel reserve no longer exists. If Par Hawaii reduces output or closes, every barrel of replacement fuel must arrive by ocean vessel through supply chains the Hormuz crisis has disrupted. The contingency plan is to bid for tanker cargoes in a global market where every buyer is scrambling for the same barrels.

The DoD knows its fuel supply chains. DLA-Energy manages supplier relationships across every region. To our understanding, what no institution has done is assess the resilience of these supply chains against the trends this analysis describes: fleet contraction, export redirection, refinery closures. And no institution has modeled what military priority invocation under the Defense Production Act would mean for civilian fuel availability in the same regions.

The dependency between military and civilian fuel supply is structural.

V. The Illusion Exposed

The Gulf Coast looked resilient because surplus refining capacity substituted for institutional attention. The Hormuz crisis revealed what happens when that capacity is stressed, and no institution has defined what adequate domestic coverage requires.

The statutory authorities exist. But the lesson of the Hormuz crisis is not that someone should have exercised these authorities sooner. The lesson is that domestic fuel supply adequacy has been left undefined, and as a result, no capacity to monitor the risk was ever built. Proactive understanding and prevention, not response, is the gap the crisis has exposed.

The gap is national. The attention deficit runs from the refineries of Beaumont and Port Arthur to the tank farms of Los Angeles. From Travis Air Force Base to Pearl Harbor. At none of these points does one individual institution hold the mandate and the data to determine whether domestic fuel supply is adequate for what the country actually needs.

To see the scale of this vacuum in practice, one only needs to look at the current mandates of key stakeholders:

State energy commissioners:

Check whether your most recent Integrated Resource Plan or fuel supply assessment includes a line item for the domestic-export balance at the refineries that serve your state.

Utility planners serving military installations:

Ask whether DLA-Energy has mapped the civilian supply chain dependencies for the bases in your service territory.

Gulf Coast refinery operators:

Ask your own government affairs teams whether a single compliance memo in the last decade has addressed domestic supply obligation.

If no institution is assessing the Gulf Coast refining surplus, the question this series turns to next is: Who is assessing fuel supply adequacy in the regions that do not have a surplus at all?

Next in this series:

“The Undefined Risk, Domestic fuel supply adequacy has never been measured because it has never been defined”

Mothusi Pahl serves on the Advisory Council of the Alliance for Innovation and Infrastructure and on the Board of Directors of the Great Plains Institute. He is Principal at Hartwell and Loche, a strategic advisory practice focused on energy, regulated industries and commercial strategy.

Published with the Alliance for Innovation and Infrastructure (Aii). The views and opinions expressed are solely those of the author and do not necessarily reflect the views of Aii or its leadership.

© 2026 Hartwell & Loche Energy. All rights reserved.

Citations and Notes

[1] BIC Magazine, “Gulf Coast refiners and chemical plants adapt strategies as markets reset,” February 2026. https://www.bicmagazine.com/industry/refining-petrochem/gulf-coast-refiners-chemical-plants-adapt-strategies-markets-reset/

[2] U.S. Energy Information Administration, “Maritime exports of petroleum products increased in January 2026,” Today in Energy. https://www.eia.gov/todayinenergy/detail.php?id=67184

[3] BIC Magazine, “Gulf Coast refineries face margin squeeze as crude prices tumble,” January 2026. Gulf Coast refineries process approximately 55% of national capacity. https://www.bicmagazine.com/industry/refining-petrochem/gulf-coast-refineries-face-margin-squeeze/

[4] U.S. Energy Information Administration, “Amid regional conflict, the Strait of Hormuz remains critical oil chokepoint.” https://www.eia.gov/todayinenergy/detail.php?id=65504

[5] Wikipedia, “2026 Strait of Hormuz crisis.” Pre-crisis Brent: Capital.com, March 2026 (“Brent ended 2025 at $60.92”). https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis

[6] Standard industry reference. Fortune/Reuters, “Hurricane Harvey Knocked Out Over 10% of U.S. Oil Refining Capacity,” August 28, 2017. https://fortune.com/2017/08/28/hurricane-harvey-oil-refining/

[7] EIA, PADD 3 Exports of Finished Petroleum Products (monthly data). Computed averages: 2009: 1,280.5 kb/d; 2025: 2,724.0 kb/d. https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?f=m&n=pet&s=mtpexp32

[8] America First Refining press release, March 10, 2026; Port of Brownsville announcement, March 11, 2026. Previously permitted as Element Fuels Holdings, LLC (2024). https://www.prnewswire.com/news-releases/america-first-refining-secures-landmark-20-year-offtake-agreement-and-capital-investment-to-construct-first-new-us-refinery-in-50-years-302710137.html

[9] KXAN, “Brownsville oil refinery announces new funding partner,” March 2026. Reliance invested as minority partner with offtake agreement to purchase at least 80% of product. https://www.kxan.com/news/texas-politics/brownsville-oil-refinery-announces-new-funding-partner-anticipates-april-groundbreaking/

[10] Congressional Research Service, “Crude Oil Exports and Related Provisions in P.L. 114-113,” R44403. https://crsreports.congress.gov/product/pdf/R/R44403

[11] Congressional Research Service, “The International Emergency Economic Powers Act,” R43442. https://crsreports.congress.gov/product/pdf/R/R43442

[12] 10 CFR Part 221, “Priority Supply of Crude Oil and Petroleum Products to the Department of Defense Under the Defense Production Act.” https://www.ecfr.gov/current/title-10/chapter-II/subchapter-A/part-221

[13] Export Administration Regulations, Bureau of Industry and Security. Refined petroleum products are classified EAR99: no license required.

[14] KBTX, “President Trump announces first new U.S. oil refinery in 50 years,” March 11, 2026. America First Refining previously operated under the name Element Fuels Holding, LLC. https://www.kbtx.com/2026/03/11/president-trump-announces-first-new-us-oil-refinery-50-years-port-brownsville/

[15] U.S. Department of Energy via CNBC, March 14, 2026. SPR capacity: 714 million barrels. https://www.cnbc.com/2026/03/14/iran-war-iea-oil-stockpile-spr-strait-hormuz.html

[16] IEA, “Japan Oil Security Policy.” The Oil Stockpiling Act requires 70 days of domestic consumption for industry stocks. METI has the power to conduct on-site inspections; penalties include imprisonment. https://www.iea.org/articles/japan-oil-security-policy

[17] GlobalSecurity.org, “DLA Energy Americas.” Distribution from “strategic refineries, primarily on the West and Gulf Coasts.” See also CRS R40459. https://www.globalsecurity.org/military/agency/dod/desc-am.htm

[18] Par Pacific Holdings. https://www.parpacific.com/operations/hawaii

[19] USNI News, “JTF-Red Hill Turns Over Remaining Fuel Depot Closure Tasks to the Navy,” March 29, 2024. Defueling completed March 6, 2024. https://news.usni.org/2024/03/29/jtf-red-hill-turns-over-remaining-fuel-depot-closure-tasks-to-the-navy