This is part of a series on electric utilities in the United States. Follow along to learn more about both electric infrastructure and markets.

We are witnessing the “iPhone moment” of the American power grid. For most of the last century, the electric system functioned like a landline: fixed, centralized, and one-directional. Power flowed from large plants through transmission networks to end-users who simply consumed it.

That energy system model still underpins today’s grid. But as of 2026, it is evolving into a dynamic, two-way network driven by five forces:

- Distributed Energy Resources (DERs) at the edge of the grid: enabling real-time load control

- Renewable-centered generation, reducing dependence on fossil-fuels

- Energy Storage Systems (ESS), flattening peak cost dynamics

- Electrification of buildings and transport, increasing demand peak, yearly sales volume, and yearly revenue

- Prosumerism, increasing supply-chain economic opportunity for energy balancing

At the center of this transition is a changing resource mix that can be understood in terms of three functional roles.

First, fossil-fuel generation remains the backbone of reliability. These dispatchable resources balance real-time demand and often set wholesale prices during peak periods. However, they face fuel volatility, high marginal costs, and emissions constraints. In some regions, nuclear energy also provides consistent electricity.

Second, renewable energy (primarily wind and solar) is reshaping the supply curve. With near-zero marginal cost, renewables suppress prices when available. Their growth – from less than 1 percent of generation in 2005 to roughly 19 percent in 2025 – has materially shifted market dynamics. However, their output depends on weather, creating potential mismatches between supply and demand.

Third, generation-scale storage bridges the gap. Batteries and other storage technologies shift energy across time – absorbing excess supply and discharging during constraints. This supports reliability, improves market efficiency, and enables higher renewable penetration. U.S. storage capacity – predominantly utility-scale – reached 37.4 gigawatts by late 2025, with further expansion underway.

This increasingly flexible, renewable-centered system extends beyond large-scale generation. A parallel shift is occurring at the grid edge. Homes, businesses, and industrial sites are becoming active participants. Rooftop solar generates power behind the meter. Residential batteries make that energy dispatchable over time, functioning as behind-the-meter storage that optimizes consumption. Electric vehicles introduce large, flexible loads. Smart devices adjust usage in response to price or grid conditions. These technologies – collectively known as distributed energy resources (DERs) – transform demand from fixed to flexible.

In addition to DERs, energy storage systems (ESS) across generation, transmission, distribution, and customer levels are central to this shift. Historically, the grid’s design model is to chase the forecasted peak demand so that infrastructure is constructed just in time. The peak occurs relatively few hours each year when consumption is highest, resulting in infrastructure that is often underutilized but costly. Storage changes that equation. By enabling flow and economic peak flattening across bulk markets, grid infrastructure, and end-user demand, the system dynamic can be used to smooth peaks rather than continuously build for them. Smoother peaks require lower delivery and supply costs to maintain balance.

Electrification adds another layer of complexity. Electric vehicles (EVs), heat pumps, and industrial electrification are increasing total demand and raising peak demand higher. At the same time, many of these loads are flexible. EV charging, for example, can shift across multi-hour windows to align with system conditions. This creates a paradox: electrification increases consumption throughout the peak day while also enabling optimization of when the system-wide consumption occurs.

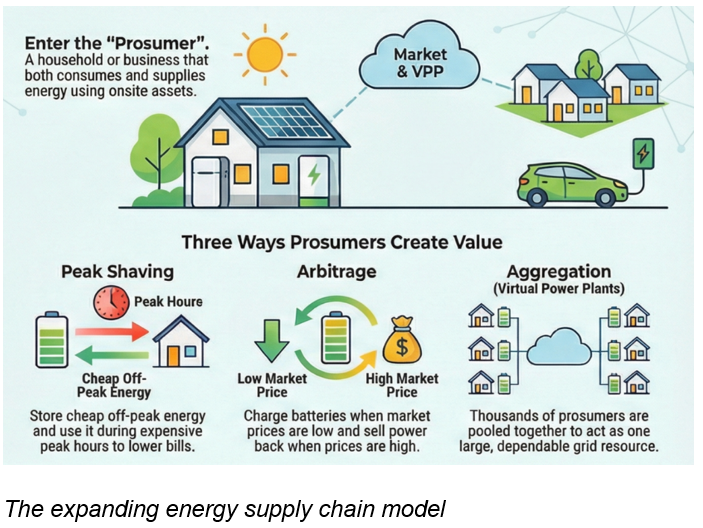

These dynamics challenge a core assumption of the traditional grid: that consumers are passive. In the emerging model, they become “prosumers,” both consuming and producing electricity, providing new value to the dynamic. A home with solar and storage can reduce or reverse net demand. A commercial building can curtail load during system stress. A fleet of EVs can align charging with renewable output. Individually small, these actions become system-shaping when adopted at scale.

When coordinated, these distributed resources form a virtual power plant (VPP), a software-driven aggregation of assets that can be monitored and dispatched as a single unit.

During system stress, this network responds by dispatching aggregated behind-the-meter storage, reducing load, and exporting generation. From the operator’s perspective, this is equivalent to a conventional plant coming online, without new infrastructure.

This has direct cost implications. By reducing peak demand, VPPs can lower the need for additional transmission and distribution investment, easing pressure on delivery charges. Reduced reliance on the most expensive marginal generators can also lower supply costs.

Scaling depends on regulatory and technological enablers. On the regulatory side, FERC Order No. 2222 marked a major inflection point. It requires wholesale electricity markets to allow aggregated DERs to participate alongside traditional generators, opening new revenue streams and operational roles for distributed resources. On the technological side, software is essential. Managing thousands of distributed devices requires real-time monitoring, forecasting, and dispatch, more akin to managing air traffic than operating a single plant. Coordination must also respect local distribution constraints, ensuring that increased flexibility does not create new bottlenecks.

This shift is still emerging, but progress is already visible. Grid operators such as the New York Independent System Operator (NYISO) and the California Independent System Operator (CAISO) are implementing frameworks that allow DER aggregations to participate in wholesale markets. Utilities in states like Texas are piloting residential battery programs that can deliver meaningful peak capacity. Industry estimates suggest that U.S. VPP capacity grew significantly between 2024 and 2025, an early signal of scaling potential.

At its core, this transition changes how the system thinks about demand. The traditional model builds infrastructure for worst-case scenarios. The emerging model manages peak demand through coordination and flexibility.

This progression in the dynamic can be understood as:

- Peak Chasing: Building for worst-case demand

- Peak Reduction: Lowering local behind-the-meter demand

- Peak Shaving: Reducing localized and system-wide demand during stressed hours

- Load Shifting: Moving energy consumption to lower-cost periods

- Flattening: Smoothing demand over the peak period to reduce extremes towards the average consumption

Even incremental progress reduces system strain and cost.

The benefits are broad. Reliability improves as coordinated distributed resources reduce peak stress. Consumers benefit through lowered direct and indirect costs. Prosumers gain access to new revenue streams. Emissions decline as reliance on high-cost, high-emission peaker plants are decreased in supply selection.

At the same time, complexity in the dynamic increases. Distribution systems were not designed for two-way power flows. Planning becomes more difficult when demand is dynamic and partially controllable. Utility business models, historically built around infrastructure investment, must adapt to a world where some of that infrastructure can be deferred.

What is emerging is not yet a fully bidirectional grid, but a transitional hybrid:

- Power Flow: Localized, increasingly bidirectional flows emerge as distributed energy resources (DERs) both consume from and export power back to the grid.

- Operations: Control centers begin coordinating with DER aggregators, introducing more dynamic, distributed management of supply, demand, and local constraints.

- Economics: Pricing and incentives become more dynamic, reflecting localized conditions and enabling new value streams from flexibility, load shifting, and distributed participation.

The centralized system remains the foundation. Large generators and transmission still carry most of the load. But layered on top is something fundamentally new: a distributed, digital, and flexible network at the grid edge.

The next question is what happens when this transition is complete – and how to get there?

Written by Ildi Telegrafi, Policy Fellow and Jackson Murray, Public Policy Intern

The Alliance for Innovation and Infrastructure (Aii) is an independent, national research and educational organization working to advance innovation across industry and public policy. The only nationwide public policy think tank dedicated to infrastructure, Aii explores the intersection of economics, law, and public policy in the areas of climate, damage prevention, eminent domain, energy, infrastructure, innovation, technology, and transportation.